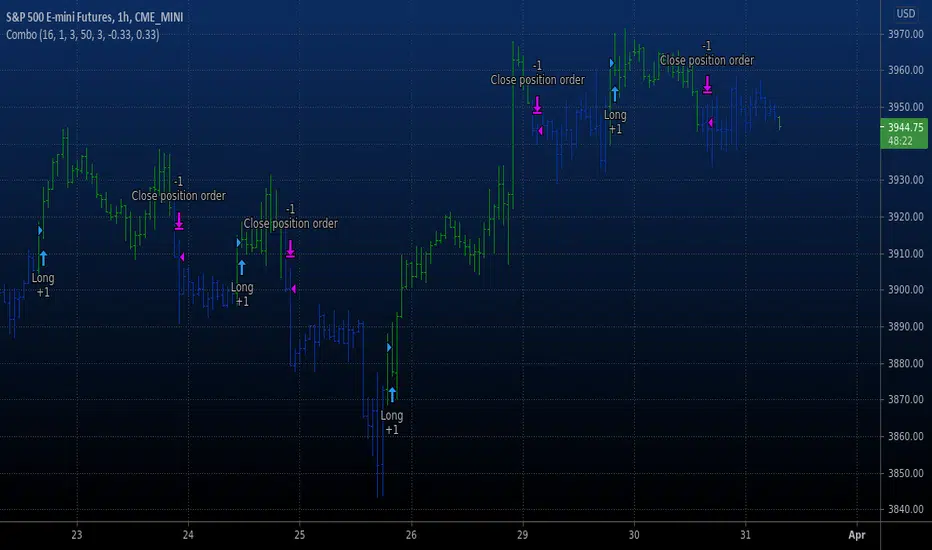

Scalping Dips On Trend (by Coinrule)Coinrule's Community is an excellent source of inspiration for our trading strategies.

In these months of Bull Market, our traders opted mostly on buy-the-dips strategies, which resulted in great returns recently. But there has been an element that turned out to be the cause for deep division among the Community.

Is it advisable or not to use a stop-loss during a Bull Market?

This strategy comes with a large stop-loss to offer a safer alternative for those that are not used to trade with a downside protection.

Entry

The strategy buys only when the price is above the Moving Average 50 , making it less risky to buy the dip, which is set to 2%.

The preferred time frame is 1-hour.

The stop-loss is set to be quite loose to increase the chances of closing the trade in profit, yet protecting from unexpected larger drawdowns that could undermine the allocation's liquidity.

Exit

Stop loss: 10%

Take Profit: 3%

In times of Bull Market, such a trading system has a very high percentage of trades closed in profit (ranging between 70% to 80%), which makes it still overall profitable to have a stop-loss three times larger than the take profit.

Pro tip: use a larger stop-loss only when you expect to close in profit most of the trades!

The strategy assumes each order to trade 30% of the available capital and opens a trade at a time. A trading fee of 0.1% is taken into account.

在腳本中搜尋"the strat"

Combo Backtest 123 Percent change bar This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This histogram displays price or % change from previous bar.

WARNING:

- For purpose educate only

- This script to change bars colors.

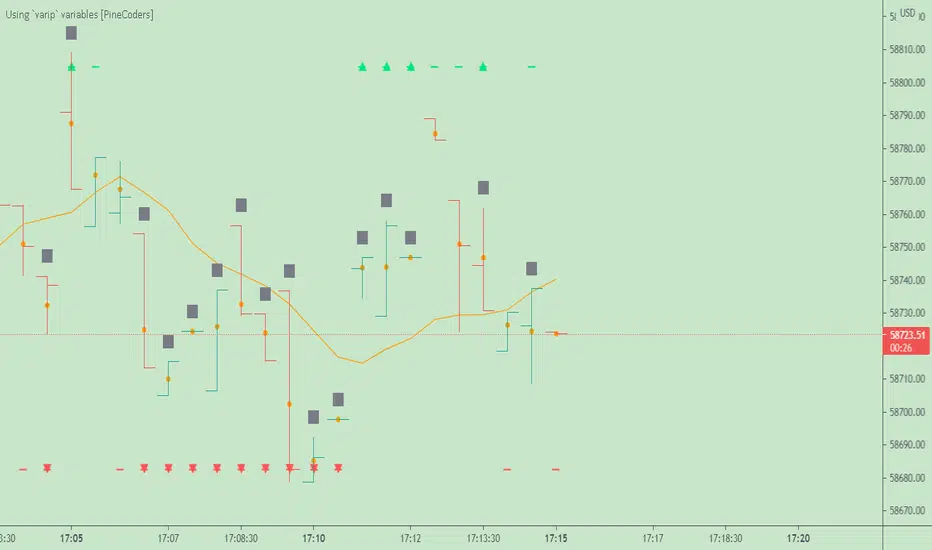

Using `varip` variables [PineCoders]█ OVERVIEW

The new varip keyword in Pine can be used to declare variables that escape the rollback process, which is explained in the Pine User Manual's page on the execution model . This publication explains how Pine coders can use variables declared with varip to implement logic that was impossible to code in Pine before, such as timing events during the realtime bar, or keeping track of sequences of events that occur during successive realtime updates. We present code that allows you to calculate for how much time a given condition is true during a realtime bar, and show how this can be used to generate alerts.

█ WARNINGS

1. varip is an advanced feature which should only be used by coders already familiar with Pine's execution model and bar states .

2. Because varip only affects the behavior of your code in the realtime bar, it follows that backtest results on strategies built using logic based on varip will be meaningless,

as varip behavior cannot be simulated on historical bars. This also entails that plots on historical bars will not be able to reproduce the script's behavior in realtime.

3. Authors publishing scripts that behave differently in realtime and on historical bars should imperatively explain this to traders.

█ CONCEPTS

Escaping the rollback process

Whereas scripts only execute once at the close of historical bars, when a script is running in realtime, it executes every time the chart's feed detects a price or volume update. At every realtime update, Pine's runtime normally resets the values of a script's variables to their last committed value, i.e., the value they held when the previous bar closed. This is generally handy, as each realtime script execution starts from a known state, which simplifies script logic.

Sometimes, however, script logic requires code to be able to save states between different executions in the realtime bar. Declaring variables with varip now makes that possible. The "ip" in varip stands for "intrabar persist".

Let's look at the following code, which does not use varip :

//@version=4

study("")

int updateNo = na

if barstate.isnew

updateNo := 1

else

updateNo := updateNo + 1

plot(updateNo, style = plot.style_circles)

On historical bars, barstate.isnew is always true, so the plot shows a value of "1". On realtime bars, barstate.isnew is only true when the script first executes on the bar's opening. The plot will then briefly display "1" until subsequent executions occur. On the next executions during the realtime bar, the second branch of the if statement is executed because barstate.isnew is no longer true. Since `updateNo` is initialized to `na` at each execution, the `updateNo + 1` expression yields `na`, so nothing is plotted on further realtime executions of the script.

If we now use varip to declare the `updateNo` variable, the script behaves very differently:

//@version=4

study("")

varip int updateNo = na

if barstate.isnew

updateNo := 1

else

updateNo := updateNo + 1

plot(updateNo, style = plot.style_circles)

The difference now is that `updateNo` tracks the number of realtime updates that occur on each realtime bar. This can happen because the varip declaration allows the value of `updateNo` to be preserved between realtime updates; it is no longer rolled back at each realtime execution of the script. The test on barstate.isnew allows us to reset the update count when a new realtime bar comes in.

█ OUR SCRIPT

Let's move on to our script. It has three parts:

— Part 1 demonstrates how to generate alerts on timed conditions.

— Part 2 calculates the average of realtime update prices using a varip array.

— Part 3 presents a function to calculate the up/down/neutral volume by looking at price and volume variations between realtime bar updates.

Something we could not do in Pine before varip was to time the duration for which a condition is continuously true in the realtime bar. This was not possible because we could not save the beginning time of the first occurrence of the true condition.

One use case for this is a strategy where the system modeler wants to exit before the end of the realtime bar, but only if the exit condition occurs for a specific amount of time. One can thus design a strategy running on a 1H timeframe but able to exit if the exit condition persists for 15 minutes, for example. REMINDER: Using such logic in strategies will make backtesting their complete logic impossible, and backtest results useless, as historical behavior will not match the strategy's behavior in realtime, just as using `calc_on_every_tick = true` will do. Using `calc_on_every_tick = true` is necessary, by the way, when using varip in a strategy, as you want the strategy to run like a study in realtime, i.e., executing on each price or volume update.

Our script presents an `f_secondsSince(_cond, _resetCond)` function to calculate the time for which a condition is continuously true during, or even across multiple realtime bars. It only works in realtime. The abundant comments in the script hopefully provide enough information to understand the details of what it's doing. If you have questions, feel free to ask in the Comments section.

Features

The script's inputs allow you to:

• Specify the number of seconds the tested conditions must last before an alert is triggered (the default is 20 seconds).

• Determine if you want the duration to reset on new realtime bars.

• Require the direction of alerts (up or down) to alternate, which minimizes the number of alerts the script generates.

The inputs showcase the new `tooltip` parameter, which allows additional information to be displayed for each input by hovering over the "i" icon next to it.

The script only displays useful information on realtime bars. This information includes:

• The MA against which the current price is compared to determine the bull or bear conditions.

• A dash which prints on the chart when the bull or bear condition is true.

• An up or down triangle that prints when an alert is generated. The triangle will only appear on the update where the alert is triggered,

and unless that happens to be on the last execution of the realtime bar, it will not persist on the chart.

• The log of all triggered alerts to the right of the realtime bar.

• A gray square on top of the elapsed realtime bars where one or more alerts were generated. The square's tooltip displays the alert log for that bar.

• A yellow dot corresponding to the average price of all realtime bar updates, which is calculated using a varip array in "Part 2" of the script.

• Various key values in the Data Window for each parts of the script.

Note that the directional volume information calculated in Part 3 of the script is not plotted on the chart—only in the Data Window.

Using the script

You can try running the script on an open market with a 30sec timeframe. Because the default settings reset the duration on new realtime bars and require a 20 second delay, a reasonable amount of alerts will trigger.

Creating an alert on the script

You can create a script alert on the script. Keep in mind that when you create an alert from this script, the duration calculated by the instance of the script running the alert will not necessarily match that of the instance running on your chart, as both started their calculations at different times. Note that we use alert.freq_all in our alert() calls, so that alerts will trigger on all instances where the associated condition is met. If your alert is being paused because it reaches the maximum of 15 triggers in 3 minutes, you can configure the script's inputs so that up/down alerts must alternate. Also keep in mind that alerts run a distinct instance of your script on different servers, so discrepancies between the behavior of scripts running on charts and alerts can occur, especially if they trigger very often.

Challenges

Events detected in realtime using variables declared with varip can be transient and not leave visible traces at the close of the realtime bar, as is the case with our script, which can trigger multiple alerts during the same realtime bar, when the script's inputs allow for this. In such cases, elapsed realtime bars will be of no use in detecting past realtime bar events unless dedicated code is used to save traces of events, as we do with our alert log in this script, which we display as a tooltip on elapsed realtime bars.

█ NOTES

Realtime updates

We have no control over when realtime updates occur. A realtime bar can open, and then no realtime updates can occur until the open of the next realtime bar. The time between updates can vary considerably.

Past values

There is no mechanism to refer to past values of a varip variable across realtime executions in the same bar. Using the history-referencing operator will, as usual, return the variable's committed value on previous bars. If you want to preserve past values of a varip variable, they must be saved in other variables or in an array .

Resetting variables

Because varip variables not only preserve their values across realtime updates, but also across bars, you will typically need to plan conditions that will at some point reset their values to a known state. Testing on barstate.isnew , as we do, is a good way to achieve that.

Repainting

The fact that a script uses varip does not make it necessarily repainting. A script could conceivably use varip to calculate values saved when the realtime bar closes, and then use confirmed values of those calculations from the previous bar to trigger alerts or display plots, avoiding repaint.

timenow resolution

Although the variable is expressed in milliseconds it has an actual resolution of seconds, so it only increments in multiples of 1000 milliseconds.

Warn script users

When using varip to implement logic that cannot be replicated on historical bars, it's really important to explain this to traders in published script descriptions, even if you publish open-source. Remember that most TradingViewers do not know Pine.

New Pine features used in this script

This script uses three new Pine features:

• varip

• The `tooltip` parameter in input() .

• The new += assignment operator. See these also: -= , *= , /= and %= .

Example scripts

These are other scripts by PineCoders that use varip :

• Tick Delta Volume , by RicadoSantos .

• Tick Chart and Volume Info from Lower Time Frames by LonesomeTheBlue .

Thanks

Thanks to the PineCoders who helped improve this publication—especially to bmistiaen .

Look first. Then leap.

Combo Backtest 123 Overbought/Oversold This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Simple Overbought/Oversold indicator

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Negative Volume Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The theory behind the indexes is as follows: On days of increasing

volume, you can expect prices to increase, and on days of decreasing

volume, you can expect prices to decrease. This goes with the idea of

the market being in-gear and out-of-gear. Both PVI and NVI work in similar

fashions: Both are a running cumulative of values, which means you either

keep adding or subtracting price rate of change each day to the previous day`s

sum. In the case of PVI, if today`s volume is less than yesterday`s, don`t add

anything; if today`s volume is greater, then add today`s price rate of change.

For NVI, add today`s price rate of change only if today`s volume is less than

yesterday`s.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & N Bars Up This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Evaluates for n number of consecutive higher closes. Returns a value

of 1 when the condition is true or 0 when false.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & N Bars Down This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Evaluates for n number of consecutive lower closes. Returns a value

of 1 when the condition is true or 0 when false.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & MovROC (KST indicator) This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This indicator really is the KST indicator presented by Martin Pring.

the KST indicator is a weighted summed rate of change oscillator that

is designed to identify meaningful turns. Various smoothed rate of change

indicators can be combined to form different measurements of cycles.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Moving Average Envelopes This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Moving Average Envelopes are percentage-based envelopes set above and

below a moving average. The moving average, which forms the base for

this indicator, can be a simple or exponential moving average. Each

envelope is then set the same percentage above or below the moving average.

This creates parallel bands that follow price action. With a moving average

as the base, Moving Average Envelopes can be used as a trend following indicator.

However, this indicator is not limited to just trend following. The envelopes

can also be used to identify overbought and oversold levels when the trend is

relatively flat.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & MA Displaced EnvelopeThis is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Moving Average Displaced Envelope. These envelopes are calculated

by multiplying percentage factors with their displaced expotential

moving average (EMA) core.

How To Trade Using:

Adjust the envelopes percentage factors to control the quantity and

quality of the signals. If a previous high goes above the envelope

a sell signal is generated. Conversely, if the previous low goes below

the envelope a buy signal is given.

WARNING:

- For purpose educate only

- This script to change bars colors.

Basic SMA 200 StrategyThe SMA 200 basic strategy will be more than familiar to most traders.

This strategy is to stay with the programming language so to say the "Hello World" of trading.

The SMA 200 basic strategy is also one of the simplest strategies in trading. All that is required is the price and a 200 period moving average. Usually the strategy is used in the daily chart.

The rules are as follows:

Entry: A position is opened when the price crosses the moving average 200 from the bottom to the top.

Exit: The position is closed when the price crosses the moving average from top to bottom.

This is a trend following system and was originally used for trading stocks.

In my opinion, trading with the strategy is recommended to every beginner. There are strategies with better performance, but they are much more complicated to implement. And that's where the big advantage of the strategy can be seen.

Beginners are more than overwhelmed at the beginning of their trading career. Often beginners trade in the 5 min chart with 6 different indicators some signals that they have seen in a Youtube video.

Comparable to a beginner driver who immediately gets into a Porsche as his first car.

Beginners should follow simple rules and avoid intraday charts. Above all, you should do the actual work of a trader.A trader does not just press the mouse twenty times a day and then has easily earned 2000 $. A trader tests systems down to the smallest detail, optimizes and tests again, until he has found an almost " waterproof " trading system. The 200 SMA basic strategy is excellent for gaining experience, learning to follow the rules of a system and not to burn your money right away.

With this script you can test how successful the "simplest strategy in the world" would have been in the past.

Small tip: Do not trade Forex with it it will never work. The strategy is made for long trends and you can find them for example in the stock market.

Have fun with it! About a positive feedback I would be very happy of course.

Combo Backtest 123 Reversal & Money Flow Indicator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Indicator plots Money Flow Indicator (Chaikin). This indicator looks

to improve on Larry William's Accumulation Distribution formula that

compared the closing price with the opening price. In the early 1970's,

opening prices for stocks stopped being transmitted by the exchanges.

This made it difficult to calculate Williams' formula. The Chaikin

Oscillator uses the average price of the bar calculated as follows

(High + Low) /2 instead of the Open.

The indicator subtracts a 10 period exponential moving average of the

AccumDist function from a 3 period exponential moving average of the

AccumDist function.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Modified Price-Volume Trend This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The related article is copyrighted material from

Stocks & Commodities.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & MASS Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Mass Index was designed to identify trend reversals by measuring

the narrowing and widening of the range between the high and low prices.

As this range widens, the Mass Index increases; as the range narrows

the Mass Index decreases.

The Mass Index was developed by Donald Dorsey.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Martin Pring's Special K This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Pring's Special K is a cyclical indicator created by Martin Pring.

His method combines short-term, intermediate and long-term velocity

into one complete series. Useful tool for Long Term Investors

Modified for any source.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Market Facilitation Index This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Market Facilitation Index is an indicator that relates price range to

volume and measures the efficency of price movement. Use the indicator to

determine if the market is trending. If the Market Facilitation Index increased,

then the market is facilitating trade and is more efficient, implying that the

market is trending. If the Market Facilitation Index decreased, then the market

is becoming less efficient, which may indicate a trading range is developing that

may be a trend reversal.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & MACD Crossover This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

MACD – Moving Average Convergence Divergence. The MACD is calculated

by subtracting a 26-day moving average of a security's price from a

12-day moving average of its price. The result is an indicator that

oscillates above and below zero. When the MACD is above zero, it means

the 12-day moving average is higher than the 26-day moving average.

This is bullish as it shows that current expectations (i.e., the 12-day

moving average) are more bullish than previous expectations (i.e., the

26-day average). This implies a bullish, or upward, shift in the supply/demand

lines. When the MACD falls below zero, it means that the 12-day moving average

is less than the 26-day moving average, implying a bearish shift in the

supply/demand lines.

A 9-day moving average of the MACD (not of the security's price) is usually

plotted on top of the MACD indicator. This line is referred to as the "signal"

line. The signal line anticipates the convergence of the two moving averages

(i.e., the movement of the MACD toward the zero line).

Let's consider the rational behind this technique. The MACD is the difference

between two moving averages of price. When the shorter-term moving average rises

above the longer-term moving average (i.e., the MACD rises above zero), it means

that investor expectations are becoming more bullish (i.e., there has been an

upward shift in the supply/demand lines). By plotting a 9-day moving average of

the MACD, we can see the changing of expectations (i.e., the shifting of the

supply/demand lines) as they occur.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Line Regression Intercept This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Linear Regression Intercept is one of the indicators calculated by using the

Linear Regression technique. Linear regression indicates the value of the Y

(generally the price) when the value of X (the time series) is 0. Linear

Regression Intercept is used along with the Linear Regression Slope to create

the Linear Regression Line. The Linear Regression Intercept along with the Slope

creates the Regression line.

WARNING:

- For purpose educate only

- This script to change bars colors.

Buy-and-hold strategy statsWhen you develop your own strategy you should compare its performance to the "buy-and-hold" strategy (you buy the financial instrument and you hold it long term). Ideally your strategy should perform better than the buy-and-hold strategy. While the net profit % of the buy-and-hold strategy is available under the "Performance Summary" tab of the "Strategy Tester" there are other factors that should be considered though. This is where this strategy comes in. It mimics the buy-and-hold strategy and gives you all the stats that are available for any strategy. For example, one such criteria that should be considered is the max. drawdown. Even if you strategy performs worse than the buy-and-hold strategy in terms of net profit, if the max. drawdown of your strategy is considerably lower than that of the buy-and-hold it may overall be a better strategy than the buy-and-hold as, in this scenario, it likely exposes the investor to significantly less risk.

Combo Backtest 123 Reversal & Laguerre-based RSI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This is RSI indicator which is more sesitive to price changes.

It is based upon a modern math tool - Laguerre transform filter.

With help of Laguerre filter one becomes able to create superior

indicators using very short data lengths as well. The use of shorter

data lengths means you can make the indicators more responsive to

changes in the price.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Backtest 123 Reversal & Signal To Noise This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The signal-to-noise (S/N) ratio.

And Simple Moving Average.

WARNING:

- For purpose educate only

- This script to change bars colors.

EMA Crossover StrategyMoving average crossover systems measure drift in the market. They are great strategies for time-limited people.

So, why don't more people use them?

I think it's due to poor choice in choosing EMA lengths: Market Wizard Ed Seykota has a guideline for moving average crossovers: the slow line should be at least 3x the fast line. This removes a lot of the whipsaws inherent in moving average systems, which means greater profitability. His other piece of advice: long-only strategies are best in stock markets where there's a lot more upside potential.

Using these simple rules, we can reduce a lot of the whipsaws and low profitability trades! This strategy was made so you can see for yourself before trading.

=== HOW TO USE THIS INDICATOR ===

1) Choose your market and timeframe.

2) Choose the length.

3) Choose the multiplier.

4) Choose if the strategy is long-only or bidirectional.

Don't overthink the above! We don't know the best answers, that's why this strategy exists! We're going to test and find out.

After you find a good combination, set up an alert system with the default Exponential Moving Average indicators provided by TradingView.

=== TIPS ===

Increase the multiplier to reduce whipsaws (back and forth trades).

Increase the length to take fewer trades, decrease the length to take more trades.

Try a Long-Only strategy to see if that performs better.

CHOP Zone Entry Strategy + DMI/PSAR ExitThis is a Strategy with associated visual indicators and Long/Short and Reverse/Close Position Alerts for the Choppiness Index (CHOP) . It is used to determine if the market is choppy (trading sideways) or not choppy (trading within a trend in either direction). CHOP is not directional, so a DMI script was ported into this strategy to allow for trend confirmation and direction determination; it consists of an Average Directional Index (ADX) , Plus Directional Indicator (+DI) and Minus Directional Indicator (-DI) . In addition, a Parabolic SAR is also included to act as a trailing stop during any strong trends.

Development Notes

---------------------------

This indicator, and most of the descriptions below, were derived largely from the TradingView reference manual. Feedback and suggestions for improvement are more than welcome, as well are recommended Input settings and best practices for use.

www.tradingview.com

www.tradingview.com

www.tradingview.com

Recommend using the below DMI and PSAR indicators in conjunction with this script to fully visualize and understand how entry and exit conditions are chosen. Variable inputs should correlate between the scripts for uniformity and visual compatibility.

THANKS to LazyBear and his Momentum Squeeze script for helping me quickly develop a momentum state model for coloring the Chop line by trend.

Strategy Description

---------------------------

CHOP produces values that determine whether the market is choppy or trending . The closer the value is to 100 , the higher the choppiness levels , while the closer it is to 0 , the stronger the market is trending . Territories for both levels, and their associated upper and lower thresholds, are popularly defined using the Fibonacci Retracements, 61.8 and 38.2.

Basic Use

---------------------------

CHOP is often used to confirm the market condition to help you stay out of sideways markets and only enter when there is movement or imminent explosions. When readings are above the upper threshold, continued sideways movement may be expected, while readings below the lower threshold are typically indicative of a continuing trend. It is also used to anticipate upcoming trendiness changes, with the general belief that extended periods of consolidation (sideways movement) are followed by extended periods of strong, trending, directional movement, and vice versa.

One limitation in this index is that you must be cautious in deciding whether the range or trend will likely continue, or if it will reverse.

Confidence in price action and trend is higher when two or more indicators are in agreement -- while this strategy combines CHOP with both DMI and PSAR, we would still recommend pairing with other indicators to determine entry or exit trade opportunities.

Recommend also choosing 'Once Per Bar Close' when creating alerts.

Inputs

---------------------------

Strategy Direction - an option to only trade Short, Long, Both, or only in the direction of the Trend (Follow Trend is the Default).

Sensitivity - an incremental variable to test whether the past n candles are in the same trend state before triggering a delayed long or short alert (1 is the Default). Can help filter out noise and reduces active alerts.

Show Chop Index - two visual styles are provided for user preference, a visible Chop line with a background overlay, or a compact column and label only view.

Chop Lookback Period - the time period to be used in calculating CHOP (14 is the Default).

Chop Offset - changing this number will move the CHOP either forwards or backwards relative to the current market (0 is the Default).

Smooth Chop Line and Length - if enabled, the entered time period will be used in calculating a smooth average of the index (Enabled and 4 are the Defaults).

Color Line to Trend Direction - toggles whether the index line is colored to visually depict the current trend direction (Enabled is the Default).

Color Background - toggles the visibility of a background color based on the index state (Enabled is the Default).

Enable DMI Option - if enabled, then entry will be confirmed by and dependent on the ADX Key Level, with any close or reversal confirmed by both ADX and +/-DI to determine whether there is a strong trend present or not (Enabled is the Default).

ADX Smoothing - the time period to be used in calculating the ADX which has a smoothing component (14 is the Default).

DI Length - the time period to be used in calculating the DI (14 is the Default).

ADX Key Level - any trade with the ADX above the key level is a strong indicator that it is trending (23 to 25 is the suggested setting).

Enable PSAR Option - enables trailing stop loss orders (Enabled is the Default).

PSAR Start - the starting value for the Acceleration Force (0.015 is our chosen Default, 0.02 is more common).

PSAR Increment - the increment in which the Acceleration Force will move (0.001 is our chosen Default, 0.02 is more common).

PSAR Max Value - the maximum value of the Acceleration Factor (0.2 is the Default).

Color Candles Option - an option to transpose the CHOP condition levels to the main candle bars. Note that the outer red and green border will still be distinguished by whether each individual candle is bearish or bullish during the specified timeframe.

Note too that if both DMI and PSAR are deselected, then close determinations will default to a CHOP reversal strategy (e.g., close long when below 38.2 and close short when above 61.8). Though if either DMI or PSAR are enabled, then the CHOP reversal for close determination will automatically be disabled.

Indicator Visuals

---------------------------

For the candle colors, black indicates tight chop (45 to 55), yellow is loose chop (38.2 to 45 and 55 to 61.8), dark purple is trending down (< 38.2), and dark blue is trending up (> 61.8).

The background color has additional shades to differentiate a wider range of more levels…

• < 30 is dark purple

• 30 to 38.2 is purple

• 38.2 to 45 is light purple

• 45 to 55 is black

• 55 to 61.8 is light blue

• 61.8 to 70 is blue

• > 70 is dark blue

Long, Short, Close, and Reverse labels are plotted on the Chop line, which itself can be colored based on the trend. The chop line can also be hidden for a clean and compact, columnar view, which is my preferred option (see example image below).

Visual cues are intended to improve analysis and decrease interpretation time during trading, as well as to aid in understanding the purpose of this strategy and how its inclusion can benefit a comprehensive trading plan.

DMI and Trend Strength

---------------------------

To analyze trend strength, the focus should be on the ADX line and not the +DI or -DI lines. An ADX reading above 25 indicates a strong trend , while a reading below 20 indicates a weak or non-existent trend . A reading between those two values would be considered indeterminable. Though what is truly a strong trend or a weak trend depends on the financial instrument being examined; historical analysis can assist in determining appropriate values.

DMI exits trade when ADX is below the user selected key level (e.g., default is 25) and when the +/- DI lines cross (e.g., -DI > +DI exits long position and +DI > -DI exits short position).

PSAR and Trailing Stop

---------------------------

PSAR is a time and price based indicator that excels at measuring direction and duration, though not the actual strength of a trend, which is why we use this in conjunction with DMI. It is also included in this script as a trailing stop option to maximize gains during strong trends and to mitigate any false ADX strengthening signals.

This creates a parabola that is located below the candle during a Bullish trend and above during a Bearish trend. A buy or reversal is signaled when the price crosses above or below the Parabolic SAR.

Long/Short Entry

---------------------------

1. CHOP must be over 61.8 (long) or under 38.2 (short).

2. If DMI is enabled, then the ADX signal line must be above the user selected Key Level (default is 25).

3. If Sensitivity is selected, then that past candle must meet the criteria in step 1, as well as all the intermediate candles in between.

4. If "Follow Trend" is selected and PSAR is enabled, then a long position can only open when the momentum and PSAR are in an uptrend, or short when both are in a downtrend, to include all intermediate candles if the Sensitivity option is set on a past candle.

Close/Reverse

---------------------------

1. If DMI is enabled, then a close flag will be raised when the ADX signal drops below the Key Level (of 25), and -DI crosses over +DI (if long), or +DI crosses over -DI (if short).

2. If PSAR is enabled, then a close flag will be raised when the current trend state is opposite the last state.

3. If both DMI and PSAR are disabled, then a close flag will be raised if the Chop line drops under 38.2 (if long) or goes over 61.8 (if short).

4. If a Long or Short Entry is triggered on the same candle as any of the above close flags, then the position will be reversed, else the position will be closed.

Strategy Alerts

---------------------------

1. Long Entry

2. Short Entry

3. Reverse

4. Close

The provided backtest result is based on a position sizing of 10% equity with 100k initial capital. When testing SPX, disabling the DMI performed the best, but EURUSD performed poorly without it enabled, and TSLA had a small reduction in net profit. Timeframe likewise differed between commodities with TSLA performing best at 30M, SPX at 15M, and EURUSD at 4H. I do not plan on using this as a standalone strategy, but I also was expecting better results with the inclusion of EMI and PSAR to compliment the CHOP. Key elements of this script will likely be included in future, more holistic strategies.

Disclaimer

---------------------------

Past performance may not be indicative of future results. Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting. This post and the script are not intended to provide any financial advice. Trade at your own risk.

No known repainting, though there may be if an offset is introduced in the Inputs. I did my best not to code any other variables that repaint, but cannot fully attest to this fact.